By Arturo Rosales. Axis of Logic.

What started as an apparent local US problem in 2007 with risky or subprime mortgages being given to all and sundry in the US from 1996 onwards has undermined the entire western financial system.

Root of the problem

Lenders in the US bundled mortgages, both AAA rated and subprime “junk mortgages” together, and sold them on in packaged billion dollar investment vehicles (technical name for this is “securitization), stamped with top AAA ratings, to capitalist banks worldwide.

When borrowers were unable to pay and had their homes foreclosed the subprime element in the mortgage packages “infected” the rest of the mortgages bundled together since the banking institutions could not differentiate between the “good apples” and the “rotten apples” in the mortgage bundles.

The uncertainty of the real value of such mortgage bundles in light of falling house prices made these investment vehicles unsellable to other financial institutions. Banks holding these now “junk bundles” tried to claim the insurance against a possible default of these vehicles.

However, the insurance companies which had assured these investments found themselves between a rock and a hard place. Losses and claims were so large that even the world’s biggest insurance company AIG had to be bailed out by the US Treasury. The capitalist financial edifice was about to collapse under the weight of its own greed and high risk strategy.

With the banking system under threat, lending activity, the oil which lubricates the wheels of the capitalist economy, dried up sparking the deepest recession since the 1930’s Great Depression.

To summarize – the causes of the current European debt crisis are:

- Recession. In recession tax revenues fall, and governments spend more on unemployment benefits, therefore the deficit rises, increasing total debt levels.

- Bank Bailouts. In the case of Ireland, the majority of the rise in public sector debt was because the government took on the debt of private sector banks which had failed. In 2010, the Irish government spent US$64 billion to rescue the banks with public funds, causing the government to run a budget deficit equivalent to 32% of GDP in 2010. The Irish bank bailout cost roughly 30% of Irish GDP, compared to the UK bank intervention which cost roughly 6% of GDP.

- Suffering population. Increasing unemployment and underemployment, rise in poverty, diminished buying power, markets reduced for goods and services which in turn lead to...

- Sluggish Growth. Countries with sluggish growth forecasts worried government bond markets because with low growth prospects, it becomes difficult to pay back the debt.

- Housing Slump. Countries like Spain and Ireland are facing prolonged slump in house prices. This is exacerbating bank losses and diminishing prospect for growth.

- Tight Monetary Policy. Many of the peripheral EU countries lack the ability to devalue their currency because they are in the Euro. Therefore to regain competitiveness there is a need to pursue deflationary policies (cutting wages and limiting social benefits, health care, education etc). This damages growth and makes government bonds less attractive.

Note: to have enough liquidity to maintain public services, armed forces, health, education, infrastructure and so on, governments must sell debt to raise money. This money combines with tax revenues to allow governments to finance its social and debt repayment obligations. If there is a recession there is less tax revenue and so for lenders the impression is that it will be more difficult for a government to honor their debt obligations. Solution – offer higher interest rates to investors but this rebounds as there is now more money needed to service the debt.

Four years ago

In 2007, just before the financial crisis, European debt levels were relatively low by historical standards. Irish government debt was very low at around 27% of GDP. Spain was around 37% of GDP. UK debt was just over 40% of GDP.

Clearly in the case of Greece, debt was already very high before the onset of the crisis (over 100% of GDP). This gave them much less room for maneuver when tax revenues fell during the recession.

Now, however, Irish public debt is 96.2% of GDP; Spain’s is around 60.1% and the UK public debt is 80% of GDP. It is obvious that the financial situation of these countries has deteriorated in the last four years and overall, European Union (EU) public debt of all 27 countries was an average of 80% of GDP or US$12,983,000,000,000 (US$12.983 trillion).

Some explanation of debt mechanisms and their solution

Greece’s public debt was 142.8% of its GDP in 2010 and if that was not bad enough it was running an annual deficit in terms of government spending of 10.5% of GDP thus racking up more debt. EU rules stipulate that a country should not run more than a 3% budget deficit in terms of its overall annual GDP. The UK is running a deficit of 10.4%; Ireland a whopping 32.4% in relation to its GDP so it is hardly surprising that Ireland is technically bankrupt; Spain 9.2% and its Iberian neighbor, Portugal, 9.1%.

To reduce these deficits, which in the capitalist system are frowned upon since they break EU rules, governments have to save money by cutting public services as stated above. In addition, they have to generate more tax revenue and so in the end it is Joe Public who ends up paying for the mistakes and rampant greed of the bankers (banksters is more appropriate). With rising unemployment in each of these countries, the increased tax burden falls on fewer and fewer among the populace, driving taxes up even further.

This is the reason you, the readers, are witnessing mass demonstrations in Athens, Madrid and Dublin. The public is paying – so in other words in good times profits are kept in the private sector banks but in bad times the losses are passed on to the public. It’s heads I win and tails I don’t lose for the “banksters”. No wonder the public is up in arms about this massive “legalized” embezzlement of public money.

Why is Greece such a problem for the EU financial system?

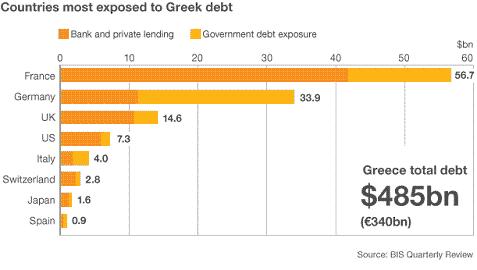

Let’s assume that Greece defaults on the money it owes. Laymen may think that this should not affect the overall EU system since Greece is a small cog in a big wheel as its economy is only equivalent to 1.89% of total EU GDP. Unfortunately it does not work like that since it depends on which banks and countries Greece owes its US$485 billion public debt.

In the EU countries have lent and borrowed money from each other and if one country gets into trouble, it cannot simply devalue its currency to get out of the problem as happened with Argentina in 2001, for example. This is because all the economies in the EU are tied together by the common currency called the euro. Now consider exposure to Greek debt by country in the chart below:

If Greece defaults, it could take France with it, for example, since France is exposed to 56.7% of the Greek debt, or US$275 billion. This could cause France to be in a position where it could not pay its own debt obligations (interest payments) on the US$2.109 trillion it owes as a country to other EU members and perhaps also to US banks.

Thus, the default of one country will cause a chain reaction throughout the EU financial system plunging banks into crisis and looking to the European Central Bank (ECB) to bail them out. Bearing in mind that the ECB holds only around US$272 billion in liquid assets for bail outs, this money would soon be swallowed up by the black hole created by countries defaulting as a chain reaction to the relatively small Greek detonation.

To quote the normally conservative BBC on this point:

“If Greece were to default, the cost of borrowing would rise for other struggling euro zone countries, forcing them to default in turn.”

One alternative would be for the ECB to start printing money to bail out the system as the Federal Reserve Bank has done in the US but by following the same strategy as the US, more money will be sloshing around in the financial system sowing the seeds of inflation which will hit the public even harder. Someone has to pay such bailouts back sooner or later but looking at the amounts involved we are not talking about “external debt” but rather “eternal debt”.

Conclusions

These are the seeds of Revolution no matter how wealthy a country is. And remember, if the euro goes down this will drag the world’s biggest economy, the European Union, into a depression involving more than 500 million people and its effects will be felt all over the planet – in the US, China, Japan, India, Brazil, Russia and other smaller economies dependent upon the liquidity of the banking system and world trade. There would be a credit crunch leading to the virtual stoppage of all global trade.

Whether the world will reach such an economic apocalypse is hard to forecast. Nevertheless, despite the loan of US$14.3 billion granted to Greece today, June 19th 2011, to allow it to meet its debt obligations in the coming months, the European situation could reach the point of no return at any time. It just needs one country to default and there are a number of candidates – Greece, Spain, Portugal, Belgium – even the UK and France both of which risk having their debt downgraded by the Rating Agencies.

All this does not just depend upon the bankers and politicians. The public is gradually reaching the end of its tether and street protests are inevitable as social spending cuts bite into the fabric of society to pay off the bankers and keep politicians in their jobs.

The “Arab Spring,” reported so heavily in the corporate/capitalist media could soon turn into a “European Summer. I doubt if such media outlets and their lackey reporters will be gloating as the masses rise up and demand justice, truth and honor –something this media cannot comprehend as they are carried about in the pockets of their capitalist paymasters.

READ HIS BIO AND MORE ESSAYS BY

AXIS OF LOGIC COLUMNIST, ARTURO ROSALES

Print This

Print This

Print This

Print This