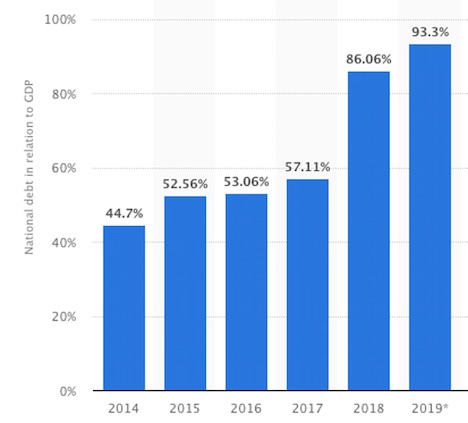

The centre left is back in control in Argentina now that Alberto Fernandez has taken office as president, succeeding the pro-market Mauricio Macri. The Peronists may have returned with an orderly transition, but Fernandez faces an economic and financial crisis and is on a collision course with the IMF. This stems from the “turbulence” of April 2018, in which the peso devalued 11% against the US dollar in less than a week amid rampant inflation, a recession, high unemployment and wider worries about emerging markets within the global economy. The Macri administration accepted an IMF bailout to the tune of US$44 billion (£33 billion), later expanded to US$57 billion. This was initially intended only as a stand-by to increase liquidity and shore up confidence around the peso, but was quickly used to repay certain debts. This was the IMF’s largest ever stand-by loan, while for Argentina it meant new debt and economic conditions from an agency that is still widely loathed in the country. No one forgets the fund’s role in the monumental crisis and default of 2001-02. It is barely a decade since the former centre-left president, Nestor Kirchner, cleared the previous IMF loans. Macri vs the Kirchners Macri’s IMF agreement was the antithesis of Kirchner’s “de-indebtedness” policy, which continued under his wife and successor Cristina Fernandez de Kirchner, who is now back as deputy president. Between 2002 and 2014, Argentina restructured and repaid its debts, agreeing a plan with 93% of the creditors who owned its sovereign bonds. This echoed previous restructurings in 1982 and 1989. The Kirchners also reduced debt denominated in foreign currency to relatively low levels – around 45% of GDP in 2014, compared to 120% in 2002 – even if these figures can partially be explained by GDP growth and a rise in local currency debt. By contrast, Macri increased this debt to well over 80% in less than four years, ahead of a “selective default” in which some debt repayments were postponed.

Certainly, the Kirchners had critics. In 2016, the Financial Times said they had bequeathed to Macri “an economy on the brink of crisis, ravaged by one of the world’s highest inflation rates”. Well, sadly this is even truer now. If 40% poverty, 56% child poverty, 60% annual inflation, a 5% decline in GDP, almost 30% youth unemployment and plummeting consumption and investment were not enough, Macri also failed in his efforts to make the country more business friendly. Argentina’s risk rating is rising and sovereign bond prices have declined sharply. Leftist policies that Macri had repudiated, such as capital and exchange controls, protectionist export tariffs and price controls, were all re-established in his final months in office. Many voters see a clear link between indebtedness and the social disaster Macri has left behind. Commodities and bonds Argentina’s difficulties are linked to the demise of the world commodity boom in 2014. A big exporter of soya and corn, the downturn has exposed the limits of Argentina’s competitiveness and its struggles to attract investment into other sectors. Relying heavily on commodities constrains Argentina’s growth potential and tends to make the peso volatile. Yet the country also suffers from local and foreign investors suddenly pulling out of its sovereign bonds and stocks when fears for the world economy rise. Under Macri’s administration, an estimated US$60 billion to US$75 billion left the country – exceeding the IMF loans. Argentina’s attraction to short-term investors was relatively simple: high risk, high gain and the carry trade – where borrowers in one country with low interest rates then lend in another with high rates. Exorbitant interest rates of 60% to 80% in pesos made Argentinian bonds attractive even with a brutal devaluation. The fact that they could get repaid very quickly by investing in the country’s 30-day bonds was an added attraction. Some bond traders may lose out now if the new government ends up defaulting properly, but don’t bet on it. Those who refused to accept a haircut in the early 2000s – the so-called vulture funds – were eventually paid back in full in 2016. The other major question is why the IMF extended new credit to the country in this situation. Even before Macri’s technical default, it had defaulted eight times in the past. According to one narrative, the economy still looked a reasonable bet until investor confidence was shaken from the Peronists winning the election. Yet even in December 2018, the fund’s review acknowledged “significant risks to debt sustainability”. The IMF lent Argentina 11 times its quota of funds available to supplement state reserves, even before the amount was increased. It delivered 80% of the committed funds in just 13 months, right before an election. It exposed 47% of the fund’s outstanding credit to a single country. The IMF probably saw an opportunity to impose strict discipline on Argentina. The loan came with the usual conditionalities: inflation targeting, tighter monetary and fiscal policy – not least a 25% cap on annual nominal wage rises, despite 60% inflation – plus budget transparency and some new anti-corruption plans. Fernandez supporters await his unveiling as president. EPA Unfortunately for the fund, the October election did not turn out as planned. It is telling that the IMF’s July report named the election as the biggest risk to debt repayments – never mind the macroeconomic imbalances in the country. Presumably the main reason why there was no fifth instalment of the loans in September was that Macri had lost the primary election in August. What next? A couple of announcements hint at how the new government will deal with the debt. The finance minister was unveiled as Martin Guzman, a close associate of the economist Joseph Stiglitz and a specialist in debt restructuring. The government has said it won’t request the final US$11 billion of the IMF’s loan. The IMF conditionalities are only binding as a means of securing the rest of this money. The government has hinted it will instead finance itself by suspending all debt repayments for two years, making clear to creditors it is no longer true that “Argentina’s capacity to repay remains adequate”. That will free around 4% of GDP a year. Will the IMF accept this? The recent social outbursts in Ecuador and Chile were also reactions to IMF programmes, so the fund might prefer not to attract more bad PR in the region. It is certainly going to be interesting to see how matters play out in the coming weeks and months. Argentina has become a new headache for the fund that it would probably rather do without. Source URL |