THE KONDRATIEFF CYCLE*

“FAR FROM THE MADDING CROWD’S IGNOBLE STRIFE…”

- THOMAS GRAY

The psychology of crowds is an interesting phenomenon best described by Gustave Le Bon in his classic ‘The Crowd’. Needless to say, the behaviour of a crowd is very different from the individuals who compose it. For our purposes, we are talking about the investor herd, but its collective behaviour differs little from the behaviour of a crowd at an English football game or that of a mob hurling rocks and abuse at a police barricade. It is not rational.

“The most striking peculiarity presented by the psychological crowd is the following: Whoever be the individuals that compose it, however like or unlike be their mode of life, their occupations, their character, or their intelligence, the fact that they have been transformed into a crowd puts them in a possession of a sort of collective mind which makes them feel, think, and act in a manner quite different from that which each individual of them would feel, think, and act were he in a state of isolation.” (The Crowd. Pages 5-6).

Or as Friedrich von Schiller put it,

“Anyone taken as an individual is tolerably sensible and reasonable-as a member of a crowd, he at once becomes a blockhead.”

‘A year after the collapse of The Mississippi bubble, the South Sea bubble ensued with horrendous losses to its investors, including Sir Isaac Newton, who famously remarked, “I can measure the motion of heavenly bodies, but not the madness of crowds.” Initially he was content to take a 100% profit on his investment, but as prices raced upwards he rejoined the party investing even more money than he had done in his initial foray. That was his mistake. When the bubble collapsed, he lost the huge amount for that time of 20,000 pounds. Even he, a very wise man, could not resist the magnetism of the mania.

Strength in numbers gives a crowd a collective feeling of confidence, indeed invincibility, which allows it to do things, which the individuals comprising it might have considered asinine. ‘The theory is, if everyone is doing it, it must be good,’ or ‘so many people just can not be wrong,’ well illustrated by the current nonbank asset backed commercial paper (ABCP) debacle. Hence the strategy of contrary investing, which proposes that when the masses are totally involved in any particular investment medium it is prudent to take an opposite tack. Such a strategy takes courage and an ability to detach oneself from the crowd.

The crowd is always dependent upon its leaders. Collectively, it displays a lack of confidence and desires its leaders to make decisions on its behalf. Le Bon put it this way, “A crowd is a servile flock, that is incapable of ever doing without a master.” (The Crowd. P.113).

“The leader has most often started as one of the led. He has himself been hypnotized by the idea, whose apostle he has since become. It has taken possession of him to such a degree that everything outside it vanishes, and that every contrary opinion appears to him an error or a superstition.” (The Crowd P.113).

The crowd’s leaders in a stock market boom are investment managers, investment advisors, stock analysts, economists and in particular the Federal Reserve Board Chairman.

According to Le Bon, affirmation, repetition and contagion are the means by which a leader instills a belief or idea in the collective mind of a crowd. “Their actions are somewhat slow, but its effects once produced are very lasting. (The Crowd. P.120). This is why it takes time for speculation to grow into a bubble.

Alan Greenspan constantly affirmed the superiority of US productivity to countenance high stock prices. Even when stock prices were reaching ridiculous levels by all past measures, stock analysts were touting that stocks were cheap or the old favourite ‘this time it’s different.’

To be really successful, affirmations must be constantly repeated and as far as possible in similar terms, such as “buy stocks for the long term.” This is always the mantra in long and prosperous bull markets. The proponents conveniently forget or do not even know that it took 25 years for stock prices to regain their 1929 highs, or that stock prices went down between 1966 and 1982.

Once affirmations have been sufficiently repeated in order to attract the attention of the crowd, contagion intervenes.

“Ideas, sentiments, emotions, and beliefs possess in crowds a contagious power as intense of that of microbes.” (The Crowd. P.122).

People do not have to be in the same place to be swept up by this contagion. Think of the worldwide demonstrations against the Iraq War. But within a crowd bound together withsimilar goals, all emotions are rapidly contagious, which explains the development of financial bubbles around the world and the suddenness of panics. This is an example from March, 1929,

“On Monday General Motors gained 2 ˝ points more, on Tuesday 3 ˝; there was great excitement as the stock crossed 150. Other stocks were beginning to be affected by the contagion as day after day the market made the front page.” (Only Yesterday. P.295).

|

“All people are most credulous when they are most happy.”

-Walter Bagehot, Editor

The Economist |

“The opinions and beliefs of crowds are especially propagated by contagion, but never by reason.”(The Crowd. P.125). This is never more evident in reckless speculation. Walter Bagehot, an editor of the Economist and renowned financial commentator of the 19th Century said, “All people are most credulous when they are most happy.”

In the latest real estate mania, affirmations were used to convince the masses that ‘real estate was still cheap’ and ‘they are not making any more land’ and that ‘mortgage interest rates would never be this low again.’ Mantras like these, constantly repeated, spawned a contagion of buying and the masses abandoned common sense in their emotional urge to own homes; in many cases not just one home , but several. Now the bubble has burst.

Once the crowd becomes totally immersed in the speculative game, it is blind to common sense and reason. It refuses to countenance any discerning views or contrary opinion. Indeed, it turns on those that reflect such dissension, by accusing them of ‘sandbagging American prosperity.’

This accusation was attached to Paul Warburg in 1929, after he advised that the orgy of speculation would lead to a disastrous collapse. But the crowd reveres its leaders, who continue to affirm the glories of being fully invested in the bull market. This crowd adulation causes some of these leaders to assume delusions of grandeur. They bask in their glory and begin to believe in their own omnipotence and sagacity.

First two articles in this series by Ian Gordon:

- THIS IS IT!

- THE CREDIT CRUNCH

Next ... "HUBRIS AND GREED"

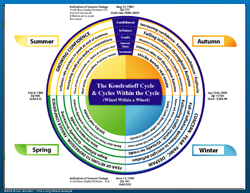

*THE KONDRATIEFF CYCLE

Spring

-

Gradual increase in business activity and employment

-

Consumer confidence increases in line with growing economy

-

Consumer prices start a gradual increase from very low levels

-

Stock prices begin a steady rise and reach a peak at the end of Spring

-

Interest rises slowly from historic low levels in line with gradual credit expansion

Summer

- Summer War – 1st Cycle: War of 1812

2nd Cycle: US Civil War

; 3rd Cycle: Word War I 1914-1918

4th Cycle: Vietnam War

- Financed by massive increase in money supply leads to large inflation which peaks at the end of Summer

- Gold prices reach significant peak at end of Summer

- Interest rates rise rapidly and peak at end of Summer

- Stock market under pressure and ends Summer with a bear market low

Autumn

-

Massive stock bull market financed by fiscal and monetary largesse

-

Stock prices reach euphonic peak to signal start of winter

-

Inflation and commodity prices fall

-

Real Estate prices rise and reach peak at beginning of winter

-

Gold and Gold equities in bear market, reach bear market low at Autumn’s end

-

Debt reaches astronomical levels by end of Autumn

-

Massive consumer confidence due to stock prices, real estate prices and plentiful jobs

Winter

-

Stocks start major bear market, the bear market is in proportion to the preceding bull market

-

Debt repudiation significant

-

Bankruptcies

-

Banks and quasi banks in crisis

-

Credit crunch – interest rates rise

-

International currency crises – a la 1931-34

-

Gold and gold equity prices rise as deflation takes hold

Print This

Print This

Print This

Print This